Explore Private Parent Loans

At Pluto, we are committed to providing unbiased and useful information to help students make their borrowing decisions. Unlike other sites, our partners cannot and do not influence our rankings or what we say about their products. We are meant to serve as a resource with some of the most information provided on each partnered lender's overview page.

Why Trust Pluto?

Private Parent Loans

More Information

It is recommended to visit each lender's overview page to gauge an in-depth understanding of that lender's terms, benefits and customizability options. For example, looking at what terms, repayment plans, graduate rewards and risk benefits can help you decide which option is best based off your individual needs. It is also encouraged to investigate each scholarship offered to help possibly lower the overall cost of college financing.

We may be paid compensation for the products offered above. This by no means influences what we say or how we portray those products. Pluto is meant to help, not hinder your education funding.

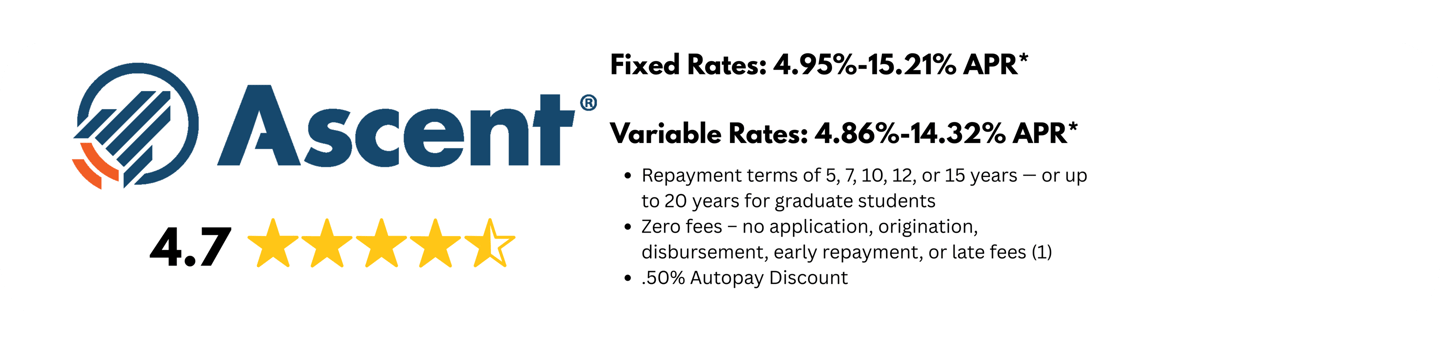

Products are organized from the lowest average fixed rate to the highest average fixed rate (for example: if a lender's fixed rates are between 4.03% -- 16.24% APR, their average fixed rate would be 10.14% because (4.03 + 16.24)/2 = 10.135). Each lender is given a number out of 5 stars as well. This number is determined based off of the amount of customizability, benefits, and rewards that could be available. However, don't let a lower number stop you if you believe that product is your best option.

How is this List Organized?

How Should I Compare?

Parent Loans: The Basics and How to Compare Your Options

Paying for college is one of the biggest financial challenges families face, and for many parents, student aid doesn’t fully cover the bill. That’s where parent loans come in. These loans allow parents to borrow money to help pay for their child’s education—but they come with responsibilities and long-term implications that are important to understand.

This article breaks down the basics of parent loans and explains how to compare them so you can make an informed decision.

What Are Parent Loans?

Parent loans are education loans taken out by a parent, not the student, to help cover college costs such as tuition, housing, books, and fees. The parent is legally responsible for repaying the loan.

The two main categories are:

Federal Parent PLUS Loans

Private Parent Loans

Each works differently in terms of eligibility, interest rates, repayment options, and borrower protections.

Federal Parent PLUS Loans: The Basics

Parent PLUS Loans are offered through the U.S. Department of Education and are available to parents of dependent undergraduate students.

Key features:

Fixed interest rate set by the federal government

Parents can borrow up to the school’s total cost of attendance (minus other financial aid)

Credit check required, but based on adverse credit history—not credit score

Eligible for federal protections like deferment, forbearance, and certain repayment plans

Pros:

Predictable fixed interest rate

Access to federal repayment and hardship options

Ability to defer payments while the student is in school

Cons:

Higher interest rates and fees than most student federal loans

Limited income-driven repayment options unless consolidated

Private Parent Loans: The Basics

Private parent loans are offered by banks, credit unions, and online lenders. Terms vary widely depending on the lender and the borrower’s credit profile.

Key features:

Fixed or variable interest rates

Interest rates based on credit score, income, and debt

Repayment terms set by the lender

Fewer borrower protections than federal loans

Pros:

Potentially lower interest rates for strong credit borrowers

More flexibility in repayment term lengths

May offer parent-to-student transfer options (in some cases)

Cons:

No federal protections or forgiveness programs

Variable rates can increase over time

Stricter credit and income requirements

How to Compare Parent Loans

Before choosing a loan, it’s important to compare offers carefully. Here are the most important factors to evaluate:

1. Interest Rates

Fixed rates stay the same for the life of the loan

Variable rates may start lower but can rise over time

Compare both the rate and whether it’s fixed or variable.

2. Fees

Look for:

Origination fees

Application fees

Late payment fees

Federal Parent PLUS Loans include an origination fee, while many private lenders do not.

3. Repayment Options

Check:

When repayment begins (immediately or after graduation)

Available repayment terms (10, 15, 20 years, etc.)

Options for deferment or forbearance during hardship

4. Borrower Protections

Federal loans generally offer:

Deferment and forbearance

Discharge in cases of death or disability

Private loans vary significantly, so read the fine print.

5. Credit Requirements

If your credit is strong, private loans may offer better rates. If not, federal Parent PLUS Loans may be more accessible despite higher costs.

6. Long-Term Impact

Consider how the loan fits into your broader financial picture:

Retirement savings

Other debts

Monthly cash flow

Borrowing for college should not jeopardize your long-term financial stability.

Final Thoughts

Parent loans can be a helpful tool for bridging the gap between college costs and available aid—but they are a serious commitment. Before borrowing, explore scholarships, grants, payment plans, and federal student loans in the student’s name.

When parent loans are necessary, comparing interest rates, fees, repayment options, and protections can make a significant difference in the total cost and stress level down the road. A well-informed choice today can protect both your family’s education goals and your financial future.

More Information

Disclosures

Ascent Disclosure:

Ascent’s undergraduate and graduate student loans are funded by Bank of Lake Mills or DR Bank, each Member FDIC.

*Ascent’s undergraduate and graduate student loans are funded by Bank of Lake Mills or DR Bank, each Member FDIC. Loan products may not be available in certain jurisdictions. Certain restrictions, limitations, terms and conditions may apply for Ascent's Terms and Conditions please visit: AscentFunding.com/Ts&Cs. Annual Percentage Rates (APRs) displayed above are effective as of 3/1/2026 and reflect an Automatic Payment Discount of 0.25% on credit-based college student loans submitted prior to 6/1/2025, a 0.5% discount for on credit-based college student loans submitted on or after 6/1/2025 and a 1.00% discount on outcomes-based loans when you enroll in automatic payments. Loans subject to individual approval, restrictions and conditions apply. Loan features and information advertised are intended for college student loans and are subject to change at any time. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions. The final amount approved depends on the borrower’s credit history, verifiable cost of attendance as certified by an eligible school and is subject to credit approval and verification of application information. Lowest interest rates require full principal and interest (Immediate) payments, the shortest loan term, a cosigner, and are only available for our most creditworthy applicants and cosigners with the highest average credit scores. Actual APR offered may be higher or lower than the examples above, based on the amount of time you spend in school and any grace period you have before repayment begins.

1) Only Ascent college loans are eligible for no fees. Ascent career training loans are subject to a one-time origination fee of 5.0% of the loan amount. All Ascent loans are eligible for no application, disbursement, late, NSF or early payment fees.

2) Ascent’s 1% Cash Back Graduation Reward is for eligible college students only and subject to terms and conditions. Eligible students must request the graduation reward from Ascent. Learn more at AscentFunding.com/CashBack. 1% Cash Back Reward amount dependent upon total loan amount for Ascent college loan borrowers. Aggregate cash back limit of $500.

3) The final ACH discount approved depends on the borrower’s credit history, verifiable cost of attendance, and is subject to credit approval and verification of application information. Automatic Payment Discount consist of 0.25% is for credit-based college student loans submitted prior to 06/01/2025, a 0.5% on credit-based college student loans submitted on or after 06/01/2025, and a 1.00% discount on outcomes-based college student loans when you enroll in automatic payments. For more information, see repayment examples or review the Ascent Student Loans Terms and Conditions.

4) Loan features, rates, and information advertised are valid and based on rates as of 1/1/2026. These are subject to change at any time, please visit our website at AscentFunding.com/Rates and AscentFunding.com/Ts&Cs for up-to-date information. Loans are subject to individual approval. Restrictions, terms, and conditions apply.

Advertising Disclosure

This site is a free online resource that strives to offer helpful content and comparison features to our visitors. We accept advertising compensation from companies that appear on the site. This does not impact the way listings and products are portrayed, the score assigned, or the order the listings and products are in. Company listings on this page DO NOT imply endorsement. We do not feature all providers on the market. Except as expressly set forth in our Terms of Use, all representations and warranties regarding the information presented on this page are disclaimed. The information, including pricing, which appears on this site is subject to change at any time. THIS IS AN ADVERTISEMENT. YOU ARE NOT REQUIRED TO MAKE ANY PAYMENT OR TAKE ANY OTHER ACTION IN RESPONSE TO THIS OFFER.